OP-ED: Ending 421-a today won’t free up $1.8B for decades

By Sean Campion

Senior Research Associate, Citizens Budget Committee

Debate in Albany and New York City on whether and how to create a successor to 421-a misses two important realities: most of the revenue would not exist absent the program; and ending the program now will not free up $1.8 billion to spend next year.

First, most development projects receiving 421-a benefits, particularly under the current version of the program, would not have been built without the incentive. Furthermore, CBC’s analysis shows that the foregone revenue will decrease by less than $100 million per year through fiscal year 2029, and it will take until fiscal year 2043 for $1 billion of the currently foregone revenue to be returned to the tax roll.

First, most development projects receiving 421-a benefits, particularly under the current version of the program, would not have been built without the incentive. Furthermore, CBC’s analysis shows that the foregone revenue will decrease by less than $100 million per year through fiscal year 2029, and it will take until fiscal year 2043 for $1 billion of the currently foregone revenue to be returned to the tax roll.

CBC analyzed the costs of seven different types of rental projects built under the current version of 421-a and found the vast majority would not be financially feasible without the 421-a tax exemption. For these projects and many others like them, there would be no incremental increase in property tax to collect absent development incentivized by the exemption.

Notably, nearly all 421-a properties pay some property taxes. The 421-a program exempts only the increase in assessed value attributable to new construction. Property owners continue to pay taxes on the assessed value of the site prior to development, a policy commonly referred to as the “mini tax.” For fiscal year 2023, CBC estimates that 421-a properties will pay $123 million in “mini tax” property taxes.

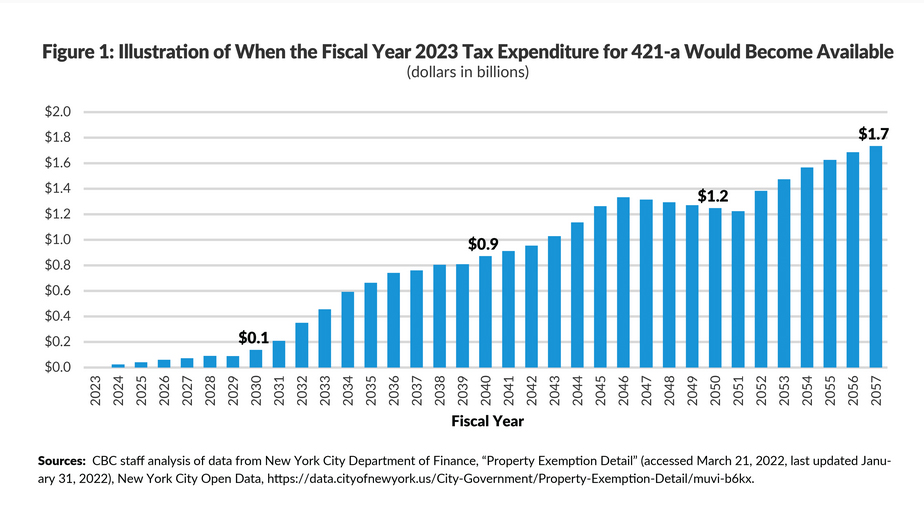

Second, ending the 421-a program will not free up $1.8 billion in tax revenue that the City could spend immediately. (See Figure 1.) Tax exemptions already granted will continue for the remainder of the term allowed at the time of the original exemption. Based on the tentative fiscal year 2023 property tax assessment roll, 60,149 tax lots are expected to receive 421-a exemptions worth over $1.7 billion in the upcoming fiscal year. These properties are at various stages in their exemption period. While some exemptions are near expiration, others, particularly those granted under the current version of 421-a, will not expire until the 2050s. (See Figure 2.)

As a result:Less than $100 million annually in foregone revenue becomes “available” over the next seven years, as foregone tax revenue decreases from $1.74 billion in fiscal year 2023 to $1.65 billion in fiscal year 2029. The “available” tax revenue averages $451 million annually from fiscal year 2030 to fiscal year 2036. The “available” annual tax revenue does not exceed $1 billion until fiscal year 2043, when the exemptions still in force decline to $700 million; and the longest exemption period is 35 years, resulting in foregone revenues through at least fiscal year 2057.

To improve affordability and catch up to past population and job growth, New York City needs to produce more housing of every kind, including both affordable and market-rate rental units. A successor to 421-a is a key component of a broader package of policies and programs needed to boost housing production, which should also include reducing construction and operating costs, increasing as-of-right zoning capacity, and reforming the property tax. Allowing 421-a to expire without a successor will result in less rental housing construction, significantly less affordable housing development (both overall and especially in high opportunity areas), and in the long run, less property tax revenue for the City.

To improve affordability and catch up to past population and job growth, New York City needs to produce more housing of every kind, including both affordable and market-rate rental units. A successor to 421-a is a key component of a broader package of policies and programs needed to boost housing production, which should also include reducing construction and operating costs, increasing as-of-right zoning capacity, and reforming the property tax. Allowing 421-a to expire without a successor will result in less rental housing construction, significantly less affordable housing development (both overall and especially in high opportunity areas), and in the long run, less property tax revenue for the City.

This op-ed originally ran on the Citizen Budget Commission blog, “No Windfall,” on May 5. The CBC is a non-partisan, nonprofit organization that pursues constructive change in the finances and services of New York City and State.